Iran War Oil Shock Reshapes Canadian Energy Market

The 2026 Iran war has produced what the International Energy Agency calls the largest oil supply shock in the history of global markets, slashing traffic through the Strait of Hormuz from roughly 20 million barrels per day in February to under 4 million by early April. The disruption has sent prices through triple-digit peaks, reshaped purchasing behaviour from Asian buyers, and opened a durable window of opportunity for Canadian producers of oil, LNG and liquefied petroleum gas.

For Canadian consumers, the shock has been felt at the pump, with retail gasoline prices up roughly 30 per cent from pre-war levels. For producers, the same dynamic has translated into stronger pricing, accelerated buyer interest and fresh momentum for long-stalled export infrastructure. The government's fuel excise tax suspension, effective April 20, is Ottawa's response to the consumer side of that equation.

The shock in numbers

Pre-war Strait of Hormuz traffic routinely moved approximately 20 million barrels of oil per day, representing close to one-fifth of global oil trade. Early April volumes were running at about 3.8 million barrels per day, a reduction of more than 80 per cent. Even after a formal United States-Iran ceasefire announcement on April 8, commercial ship traffic has not returned anywhere near pre-war volumes.

Brent crude, which traded near US$70 per barrel before the war, briefly topped US$100 and has since settled in the high US$90s. Natural gas prices have similarly surged, with Qatar's LNG exports disrupted by constrained tanker access. European and Asian gas markets have reflected that disruption in spot pricing volatility.

The IEA has framed the situation as historic. Even acute past shocks, including the 1973 embargo and the 1979 Iranian Revolution disruption, moved smaller percentages of global supply. The current combination of military activity, insurance market responses, and tanker availability constraints has amplified the impact well beyond what the physical volumes alone would suggest.

The Canadian producer advantage

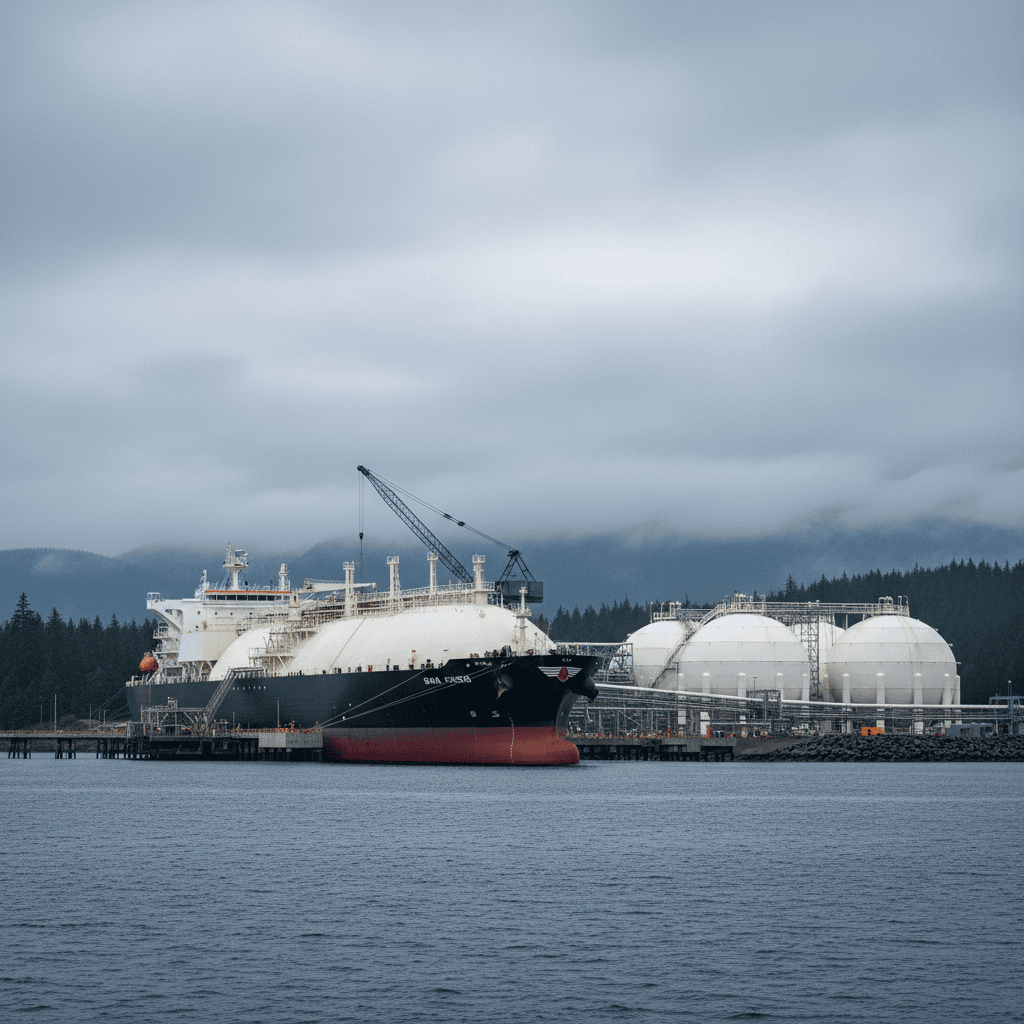

Canadian oil and gas producers have stepped into the resulting gap. With Middle East supply uncertain and Asian buyers actively seeking diversification, Canadian LNG, LPG and conventional oil exports have gained market share. Pricing on incremental volumes has been strong, and Canadian LNG projects in British Columbia have benefited from heightened buyer interest.

LNG Canada's Kitimat facility continues to ramp, and subsequent projects, including Woodfibre LNG near Squamish and Cedar LNG in northern British Columbia, remain on track to add further capacity over the next two years. Industry analysts estimate Canadian LNG could add roughly 5.4 million tonnes per annum of capacity over that window, meaningful incremental supply at a moment when Qatar has lost roughly 12.8 million tonnes per annum.

Canadian oil sands producers and conventional oil operators have also benefited from the pricing environment. Western Canadian Select differentials narrowed as North American export infrastructure worked near capacity, and cash flows to producers have improved markedly. That improvement has flowed into provincial royalty revenues in Alberta and Saskatchewan and into federal corporate tax receipts.

The consumer side

For households, the supply shock has shown up directly at the pump. Gasoline prices across major Canadian markets rose roughly 30 per cent between late February and mid-April, with regional variations running higher in Atlantic Canada and the North. Diesel and home heating oil have seen similar pressure, with particular consequences for long-haul freight, agriculture and northern communities dependent on fuel-powered generation.

The federal response, a suspension of the fuel excise tax from April 20 to September 7, is expected to cut roughly 10 cents per litre from gasoline and 4 cents from diesel. Provinces have not yet widely followed suit with their own tax relief, although pressure from affordability advocacy groups is building.

The Bank of Canada has factored the oil shock into its inflation outlook. Headline inflation has ticked up in recent prints, reflecting energy pass-through into food, shipping and construction costs. The Bank has signalled that its policy decisions will weigh those imported price pressures against softening domestic growth.

Strategic implications

The shock has crystallised long-running arguments about Canadian energy strategy. Advocates of expanded pipeline and LNG export capacity have pointed to the current moment as validation of the case for more Canadian export optionality, while critics have argued that the response to such shocks should be accelerated investment in electrification and transport alternatives.

Ottawa's stance has been pragmatic. The Carney government has emphasised that Canadian energy exports are part of global energy security, and that accelerating permitting for export infrastructure is consistent with climate objectives if paired with emissions management. The government's push for one-project, one-review approvals and for the federal-provincial energy corridor framework reflects that positioning.

Critics, including climate policy organisations and some First Nations, have argued that infrastructure decisions being accelerated during an acute crisis risk locking in emissions trajectories over decades. That debate is active in specific project files, including several under review in British Columbia, Alberta and Manitoba.

Asian market shifts

The most consequential Canadian opportunity is in Asian markets. Japanese, Korean and Chinese buyers have traditionally sourced significant volumes of LNG and oil from the Gulf. The disruption has prompted active buyer diversification, with North American and Australian suppliers, alongside emerging African producers, picking up portions of the displaced volumes.

Canadian LNG has structural advantages in the Asian market. The Pacific coast export location provides shorter shipping routes and lower freight costs compared with Gulf of Mexico exports transiting Panama. Canadian natural gas pricing, particularly from Montney and Duvernay formations, remains competitive against other supply basins.

Commercial contracts signed in recent weeks suggest the shift is more than temporary. Multi-year offtake agreements have been priced to reflect buyer willingness to pay for supply security, rather than purely for spot cost competitiveness. That structural premium on diversification is the most durable legacy of the current shock.

Political economy in Alberta and BC

For Alberta, the environment has reinforced Premier Danielle Smith's push for faster project approvals and more aggressive positioning on oil and gas exports. Bill 30, the 120-day approval law tabled this month, fits into that posture. The political logic is straightforward: if global markets are signalling demand for Canadian energy, Alberta should be the jurisdiction that can move fastest to meet it.

In British Columbia, the NDP government's posture is more balanced. Premier David Eby has supported existing LNG projects while maintaining climate commitments and engaging extensively with First Nations on consultation processes. British Columbia's approach illustrates the political challenge of balancing export opportunity with climate and Indigenous rights commitments.

Saskatchewan, home to Canada's uranium and a substantial oil producer in its own right, has been a beneficiary of both the oil price environment and the new Canada-India uranium deal. The province's budget position has improved, and Premier Scott Moe's government has framed the environment as validation of its resource-focused economic strategy.

Climate considerations

The acute shock has complicated Canada's climate policy conversation. Higher fossil fuel prices in theory improve the economics of lower-carbon alternatives, but in practice consumer tolerance for high energy prices is limited, and political pressure to reduce prices in the short term dominates.

The Liberal government has effectively paused the consumer carbon price. Industrial carbon pricing continues, but political attention has moved toward clean-tech investment credits, tax measures for electrification, and transportation decarbonisation rather than broad consumer price signals. That shift reflects the political reality of the current moment more than it signals a long-term change in direction.

Longer-term, the shock has reinforced the case for diversifying Canada's energy mix and for accelerating electrification where possible. The tension between immediate affordability pressures and structural decarbonisation remains a defining policy challenge, and it will shape debates through the summer budget cycle.

Indigenous equity in energy projects

One of the defining shifts in Canadian energy over the past several years has been the rising participation of Indigenous nations as equity partners in major projects. The Cedar LNG project near Kitimat is majority-owned by the Haisla Nation, and the Ksi Lisims LNG proposal in northwestern British Columbia includes the Nisga'a Nation as a founding partner. Indigenous equity ownership, supported by the federal Canada Infrastructure Bank and by provincial loan guarantee programs, has become a structural feature of the landscape.

The current market environment strengthens the economic case for Indigenous equity positions in new energy infrastructure. With stronger pricing, clearer customer demand and faster regulatory paths emerging in Alberta and British Columbia, the prospective returns on equity investments have improved. Indigenous governments and financial institutions are evaluating participation structures across a growing pipeline of critical minerals, oil, gas and renewable energy projects.

That shift is not without controversy. Some Indigenous organisations remain opposed to expanded fossil fuel infrastructure on environmental and treaty rights grounds, and projects that go forward despite such opposition face litigation risk. But for nations that choose equity partnerships, the current market is producing opportunities that could meaningfully change long-term fiscal capacity and self-determination in resource-rich regions of the country.

What's next

Whether Strait of Hormuz traffic normalises over the coming months will be the single largest variable. Current ceasefire arrangements between Iran and the United States remain fragile, and even limited additional escalation could push prices higher again. Canadian monetary and fiscal policy responses remain calibrated to that uncertainty.

For Canadian producers, the near-term opportunity is to lock in customer relationships that will outlast the immediate shock. LNG offtake agreements, uranium supply contracts, and oil export commitments being signed now embed Canadian energy into buyer portfolios in ways that will persist even when markets normalise.

For Canadian consumers, relief from the fuel excise tax suspension will soften the impact through the summer. Beyond September, if energy prices remain elevated, political pressure on Ottawa and the provinces for additional affordability measures will grow. The durability of the current shock, and its consequences for Canadian households and industries, will be one of the defining storylines of the rest of the year.

Spotted an issue with this article?