Iran War Sends Oil Soaring, Squeezing Canadian Households

A war that began thousands of kilometres from Canada is now showing up in Canadian gas tanks, grocery bills and mortgage calculations. The conflict involving Iran, which ignited with joint United States and Israel strikes on Iranian targets on 28 February 2026, has continued to roil global energy markets through the spring, and the resulting surge in oil prices has rippled directly into the cost of living for households across the country. For a nation that is both a major energy producer and a country of commuters and consumers, the war has exposed an uncomfortable double edge.

The numbers tell the story of a sudden shock. Brent crude, the international benchmark, climbed from around US$72 a barrel in late February to nearly US$120 at its peak, a rise of more than 50 per cent in a matter of weeks. By late April the market remained elevated, with U.S. crude trading around US$107 a barrel and Brent near US$118. Those figures translate, with a lag, into higher prices at the pump and higher costs for everything that moves by truck, rail, ship or plane.

The effect on Canadian inflation has been swift. Consumer prices rose to about 2.8 per cent in April 2026, the highest reading in two years, with energy costs leading the climb. Energy prices were up roughly 19 per cent year over year, and transportation costs rose sharply as well. For families already stretched by years of elevated prices, the war has delivered a fresh squeeze at exactly the moment many had hoped inflation was settling down.

How a Distant War Reached Canadian Wallets

Oil is a global commodity, and its price is set in worldwide markets that respond instantly to threats against supply. When a conflict erupts in a region that produces and ships a large share of the world's crude, traders price in the risk of disruption immediately, pushing prices higher even before any barrel is actually lost. That is the mechanism by which a war involving Iran translated almost overnight into higher costs for Canadian drivers, even though Canada produces far more oil than it consumes.

The transmission runs through the pump first. Gasoline and diesel prices track crude with only a short delay, so the spring jump in oil quickly fed into what Canadians paid to fill up. From there the effect spreads. Higher diesel costs raise the price of trucking, which raises the cost of delivering food and consumer goods. Air travel, home heating and a wide range of industrial inputs all become more expensive, broadening the inflationary impulse well beyond the gas station.

This is why a war in the Middle East can matter as much to a household in Ontario or Atlantic Canada as a domestic policy change. The integrated nature of global energy markets means that supply threats abroad are felt at home regardless of how much oil Canada itself pumps. Prime Minister Mark Carney has framed the moment as a global energy crisis, language that captures both the scale of the disruption and the difficulty any single government faces in shielding its citizens from it.

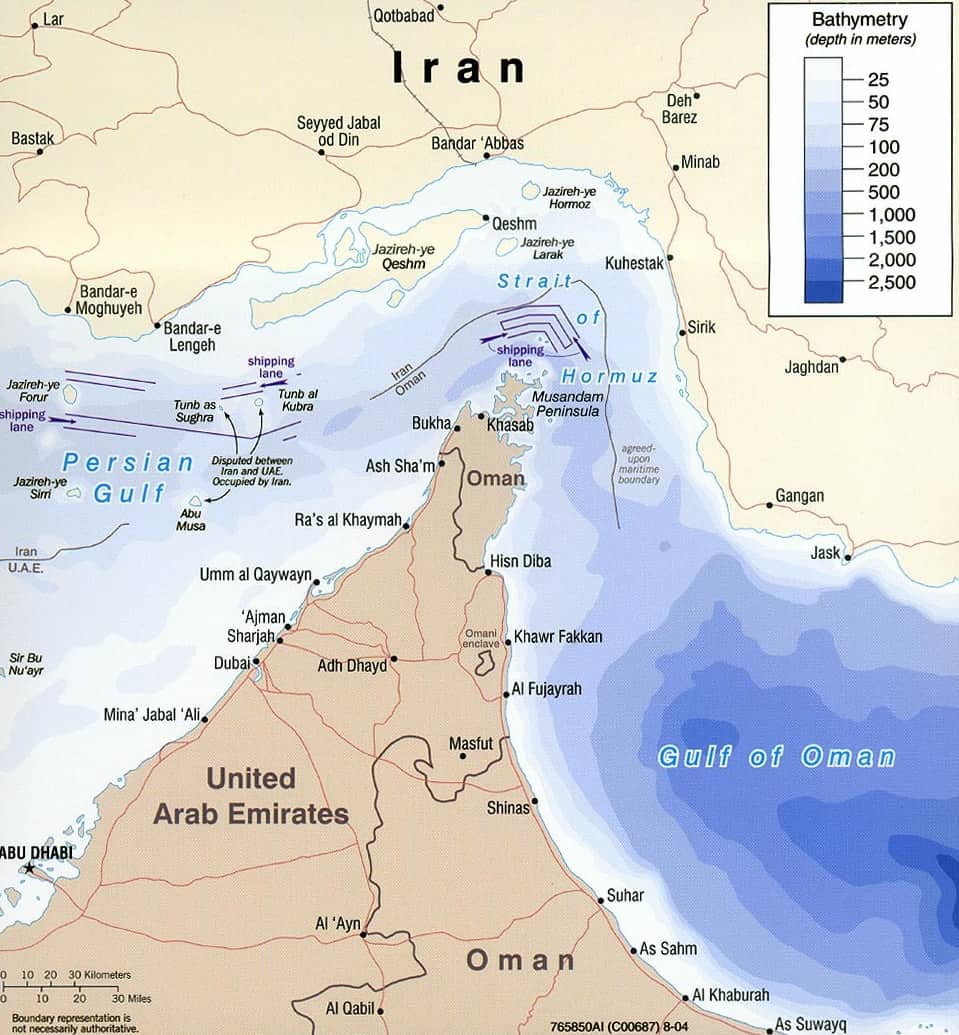

The Strait of Hormuz at the Centre of the Storm

Much of the market's anxiety has centred on a single narrow waterway. The Strait of Hormuz, the chokepoint through which a large share of the world's seaborne oil and natural gas passes, became a flashpoint after the fighting began. Around 4 March, Iran declared the strait closed, and reports of attacks on shipping followed. Initial reporting suggested that roughly a fifth of global crude oil and natural gas supply was disrupted, an extraordinary share for a single corridor.

The conflict also struck directly at energy infrastructure. Israel reportedly hit Iran's South Pars gas field, one of the largest natural gas deposits in the world, and Iran retaliated against Ras Laffan, a major energy facility in Qatar. Strikes on production and export sites raise the spectre of lasting damage to supply, not merely temporary interruptions to shipping, and markets tend to treat such attacks as especially alarming because the effects can persist long after the immediate fighting subsides.

For Canada, the strait's troubles are a reminder of how concentrated global energy logistics remain. Even though Canadian crude largely reaches market through North American pipelines and ports rather than through Hormuz, the price Canadians pay is set globally. A disruption in the Gulf therefore lands on Canadian consumers indirectly but unmistakably, lifting the benchmark prices that govern what they pay at home.

Inflation Returns as a Household Worry

The renewed climb in prices has revived a worry many Canadians had begun to set aside. After a long stretch of elevated inflation earlier in the decade, price growth had cooled, and households had started to feel some relief. The April reading of about 2.8 per cent, the highest in two years, signalled that the progress was fragile and that an external shock could quickly undo it.

Energy's outsized role in the latest figures is significant because energy costs are both highly visible and broadly felt. Few prices are as closely watched as the number on the gas station sign, and few costs touch as many parts of a household budget as fuel and heating. When energy leads inflation higher, the pain is widely shared and acutely felt, which is part of why such episodes tend to dent consumer confidence quickly.

The broader concern is that energy-driven inflation can seep into other prices over time. As transportation and input costs rise, businesses may pass them on, and persistent price pressure can begin to shape expectations. Economists watch closely for signs that a commodity shock is becoming embedded in the wider price structure, because that is far harder to reverse than a one-time jump in fuel costs.

The Bank of Canada's Difficult Balancing Act

The conflict has complicated the job of the Bank of Canada, which must weigh the inflationary effect of higher energy prices against the risk that the same shock could slow economic growth. On 29 April the central bank held its policy rate at 2.25 per cent, and its next scheduled decision falls on 10 June 2026. Between those dates, policymakers are watching the war's effect on both prices and the broader economy.

An energy shock presents central bankers with a genuine dilemma. Higher oil prices push inflation up, which would ordinarily argue for keeping interest rates elevated or raising them. Yet the same higher prices act like a tax on consumers and businesses, sapping spending power and potentially dragging on growth, which would argue for caution or even easing. The Bank must judge which force is likely to dominate, and for how long, before deciding where to set rates.

For Canadians with mortgages, lines of credit or plans to borrow, the June decision carries real weight. A central bank worried primarily about inflation may keep borrowing costs higher for longer, adding to household financial strain at a time when energy bills are already rising. A central bank more concerned about growth may move to support the economy, but at the risk of allowing price pressures to linger. The conflict has made that trade-off sharper and the path ahead less predictable.

A Windfall for Canada's Energy Heartland

The story is not one of pure pain, and that is what makes it distinctly Canadian. The same high prices that squeeze consumers deliver a windfall to the country's oil and gas producers, especially in Alberta and the oil sands. When global crude trades above US$100 a barrel, Canadian producers earn substantially more for every barrel they sell, boosting corporate revenues, provincial royalties and the broader economy of the energy heartland.

That divide places different regions of the country on opposite sides of the same event. A commuter in a large city facing higher pump prices experiences the war as a cost, while a worker, investor or government in the oil patch may see it as a boost to incomes and public finances. This is the long-standing tension of a major energy-exporting nation, where the price of oil is simultaneously a household expense and a source of national wealth.

The episode has also sharpened debates over energy security and pipeline capacity. With global supply suddenly looking vulnerable, questions about how much Canadian oil and gas can reach markets, and through what infrastructure, have taken on new prominence. Advocates of expanded capacity argue that a country with vast reserves should be better positioned to supply allies and benefit from high prices, while others stress the need to balance such ambitions against environmental and fiscal considerations.

What's Next

The immediate question is whether the conflict escalates further or begins to ease, because the answer will largely determine where oil prices, and therefore Canadian inflation, head next. Markets remain on edge over the Strait of Hormuz and the possibility of further strikes on energy infrastructure, and any fresh disruption could push prices higher again. A de-escalation, by contrast, could allow prices to retreat and relieve some of the pressure on Canadian households.

The Bank of Canada's 10 June decision will be the next concrete signpost. Policymakers will weigh the latest inflation data, the trajectory of energy prices and the war's effect on growth before setting the course for borrowing costs through the summer. Their judgment will shape mortgage payments, business investment and the broader economic mood at a delicate moment.

For Canadians, the war is a stark illustration of how tightly the domestic economy is bound to events abroad. Higher prices at the pump and at the checkout are the visible signs of a distant conflict reaching into everyday life, even as the country's energy producers reap the benefits of the same surge. How long the squeeze lasts, and how the central bank and households respond, will depend in large part on a war whose course remains far from settled.

Spotted an issue with this article?

Have something to say about this story?

Write a letter to the editor

Comments

Be the first to comment.